Introduction #

Definition of House Rental Allowance #

House Rent Allowance (HRA) is a type of financial benefit provided by an employer to its employees to cover their housing expenses. This allowance is usually a fixed amount paid as part of an employee’s salary package and is intended to help employees meet the cost of renting a place to live. The exact amount of HRA varies depending on an employee’s salary, location of residence, and other factors determined by the employer or the tax authorities. HRA is a tax-exempt benefit, which means that employees can claim exemptions on the HRA component of their salary while calculating their taxable income.

Importance of HRA in Indian Payroll #

HRA is an important component of an employee’s compensation package in India, particularly in cities where the cost of living is high. The main purpose of HRA is to help employees cover the expenses associated with renting a place to live, which is typically one of their biggest expenses.

By providing HRA as part of their salary, employers can help their employees maintain a decent standard of living, which can improve employee morale and job satisfaction. Additionally, HRA is tax-exempt, so employees can claim exemptions on the HRA component of their salary while calculating their taxable income. This can result in significant tax savings for employees, which can improve their overall financial well-being.

For employers, providing HRA can also have cost-saving benefits. By covering a portion of the employee’s housing expenses, employers can help reduce the employee’s take-home pay and thus lower the employer’s contribution to statutory benefits such as provident fund and employee state insurance.

In summary, HRA plays a crucial role in Indian payroll by providing financial support to employees to cover their housing expenses, improving employee morale and satisfaction, and providing tax benefits to both employees and employers.

Overview of HRA calculation and benefits #

The calculation of HRA in the Indian payroll is based on several factors, including the employee’s basic salary, the rent paid, and the location of the rented accommodation. The calculation of HRA is typically done based on the lowest of the following three factors:

- Actual HRA received from the employer.

- 50% of the basic salary for employees living in metro cities, or 40% of the basic salary for employees living in non-metro cities

- Actual rent paid minus 10% of the basic salary.

The employee can claim tax exemptions on the HRA received based on the lower of the actual HRA received, or the amount calculated above.

The benefits of HRA in Indian payroll include financial assistance to employees for their housing expenses, which can improve their standard of living and reduce financial stress. In addition, HRA is a tax-exempt benefit, which can provide significant tax savings to employees. For employers, providing HRA can help reduce the number of statutory benefits they need to provide to employees.

Overall, the calculation of HRA and its benefits make it a key component of the Indian payroll that provides significant financial support to employees and cost-saving benefits to employers.

Eligibility for HRA #

The eligibility for HRA in Indian payroll depends on a few factors, including the employee’s job profile, salary structure, and the location of their residence. Here are some of the key considerations for HRA eligibility:

- Job profile: Typically, employees who receive HRA in India are those who are working in the private sector or in public sector organizations that provide HRA as a part of their salary package.

- Salary structure: The amount of HRA that an employee is eligible for depends on their salary structure. HRA is typically a percentage of the employee’s basic salary, and the percentage may vary based on the employer’s policies and the location of the rented accommodation.

- Residential status: To be eligible for HRA, the employee must be a tenant and pay rent for their accommodation. If the employee owns their house, they are not eligible for HRA.

In addition to these factors, the rules and regulations governing HRA eligibility and calculation may vary based on the location of the employee’s residence and the policies of the employer. Employees need to check their eligibility for HRA and the amount they are eligible for based on their specific job profile and salary structure.

HRA Calculation #

The calculation of HRA (House Rent Allowance) in the Indian payroll is based on the following factors:

Basic salary: HRA is typically calculated as a percentage of the employee’s basic salary. The exact percentage varies depending on the employer’s policies and the location of the rented accommodation.

Location of residence: The HRA amount may vary based on the location of the employee’s rented accommodation. For example, employees living in metro cities may be eligible for a higher percentage of HRA compared to employees living in non-metro cities.

Rent paid: The actual rent paid by the employee is also a factor in HRA calculation. However, the amount of HRA that can be claimed is limited to the lowest of the following three amounts:

- Actual HRA received from the employer.

- 50% of the basic salary for employees living in metro cities, or 40% of the basic salary for employees living in non-metro cities

- Actual rent paid minus 10% of the basic salary.

Once the lowest of these amounts is determined, the employee can claim tax exemptions on this amount while calculating their taxable income.

Please visit the below link to reach the income tax site to calculate the HRA exemption https://incometaxindia.gov.in/Pages/tools/house-rent-allowance-calculator.aspx

For example, suppose an employee’s basic salary is INR 50,000, and they live in a metro city where the HRA percentage is 50%. If their actual rent paid is INR 20,000 and their HRA received from the employer is INR 18,000, then the lowest of the three amounts is INR 16,000 (50% of basic salary). The employee can claim tax exemptions on this amount while calculating their taxable income.

Employees need to check their employer’s policies and the rules and regulations governing HRA calculation in their location to determine the exact amount of HRA they are eligible for.

Benefits of HRA #

HRA, or House Rent Allowance, is a component of salary that is paid to employees to cover their rental expenses. HRA is a popular component of Indian payroll because it offers several benefits to both employees and employers. Some of the key benefits of HRA in Indian payroll include:

Tax benefits: HRA is eligible for tax exemption under Section 10(13A) of the Income Tax Act, which allows employees to claim a deduction on their taxable income for the amount spent on rent. This helps to reduce the tax liability of employees and can increase their take-home pay.

Cost savings: By providing HRA to employees, employers can save on the cost of providing housing to their employees. This is particularly beneficial for companies that operate in expensive cities where housing costs can be high.

Talent retention: Offering HRA to employees can help to retain talent and improve employee satisfaction. This is because employees can cover their housing costs more easily and can focus on their work without worrying about financial stress.

Compliance: HRA is a mandatory component of payroll in India for companies with more than 20 employees. By providing HRA, companies can ensure that they are complying with the law and avoiding any potential legal issues.

Flexibility: HRA offers flexibility to employees, as they can choose where they want to live and how much they want to spend on rent. This can help to improve employee morale and productivity.

Overall, HRA is an important component of the Indian payroll that offers several benefits to both employees and employers. By providing HRA, companies can improve compliance, reduce costs, retain talent, and enhance employee satisfaction.

Best practices for HRA administration #

When it comes to administering HRA in Indian payroll, companies should follow several best practices to ensure that the process is efficient, effective, and compliant. Here are some of the key best practices for HRA administration in Indian payroll:

Accurate documentation: Employers should maintain accurate and complete documentation related to HRA, including rental agreements, rent receipts, and HRA claim forms. This documentation should be easily accessible and organized for easy retrieval.

Clear communication: Employers should communicate the HRA policy clearly to employees, including eligibility criteria, calculation methodology, and submission procedures. This will help to avoid confusion and ensure that employees understand how to claim HRA.

Timely payments: Employers should ensure that HRA payments are made on time and comply with the agreed-upon schedule. This will help to avoid any delays or discrepancies in costs and ensure that employees receive their HRA regularly.

Regular reviews: Employers should regularly review the HRA policy to ensure that it remains relevant and competitive. This includes reviewing the rental rates and eligibility criteria to ensure that they reflect current market conditions.

Compliance with regulations: Employers should ensure that their HRA policy is compliant with all applicable laws and regulations, including tax laws and labor laws. This will help to avoid any legal issues related to HRA.

Proper record keeping: Employers should maintain proper records related to HRA payments, including employee information, payment details, and tax deductions. This will help to ensure that the company is compliant with regulatory requirements and can provide accurate records if needed.

By following these best practices, companies can ensure that their HRA administration process is efficient, effective, and compliant with all relevant regulations. This will help to improve employee satisfaction and retention, as well as the overall financial health of the company.

Challenges and drawbacks of HRA #

While HRA is a popular component of Indian payroll, there are also some challenges and drawbacks that companies should be aware of. Here are some of the key challenges and drawbacks of HRA in Indian payroll:

Eligibility criteria: One of the challenges of HRA in Indian payroll is that not all employees may be eligible for it. For example, employees who live in company-provided housing or who own their own homes may not be eligible for HRA. This can create confusion and dissatisfaction among employees who feel that they are being unfairly excluded from the benefit.

Documentation requirements: Another challenge of HRA in Indian payroll is that it requires a lot of documentation, including rental agreements and rent receipts. This can be time-consuming and difficult to manage, particularly for companies with a large workforce.

Calculation methodology: The calculation methodology for HRA can be complex, particularly in cases where employees live in shared or partially owned accommodations. This can lead to errors in calculations and disputes between employers and employees.

Tax implications: While HRA is eligible for tax exemption under certain conditions, employees may still be required to pay taxes on a portion of their HRA. This can reduce the overall benefit of HRA for employees and make it less attractive as a component of payroll.

Market fluctuations: The rental rates in India can fluctuate rapidly, particularly in metropolitan areas. This can make it difficult for companies to provide a consistent HRA benefit to employees and may lead to dissatisfaction among employees who feel that their rental costs are not being adequately covered.

Overall, while HRA can provide several benefits to employees and employers, it also comes with some challenges and drawbacks that need to be carefully managed. By understanding these challenges and drawbacks and implementing effective policies and procedures, companies can ensure that their HRA administration process is efficient, effective, and compliant.

How is House Rental Allowance (HRA) implemented in OfficePortal #

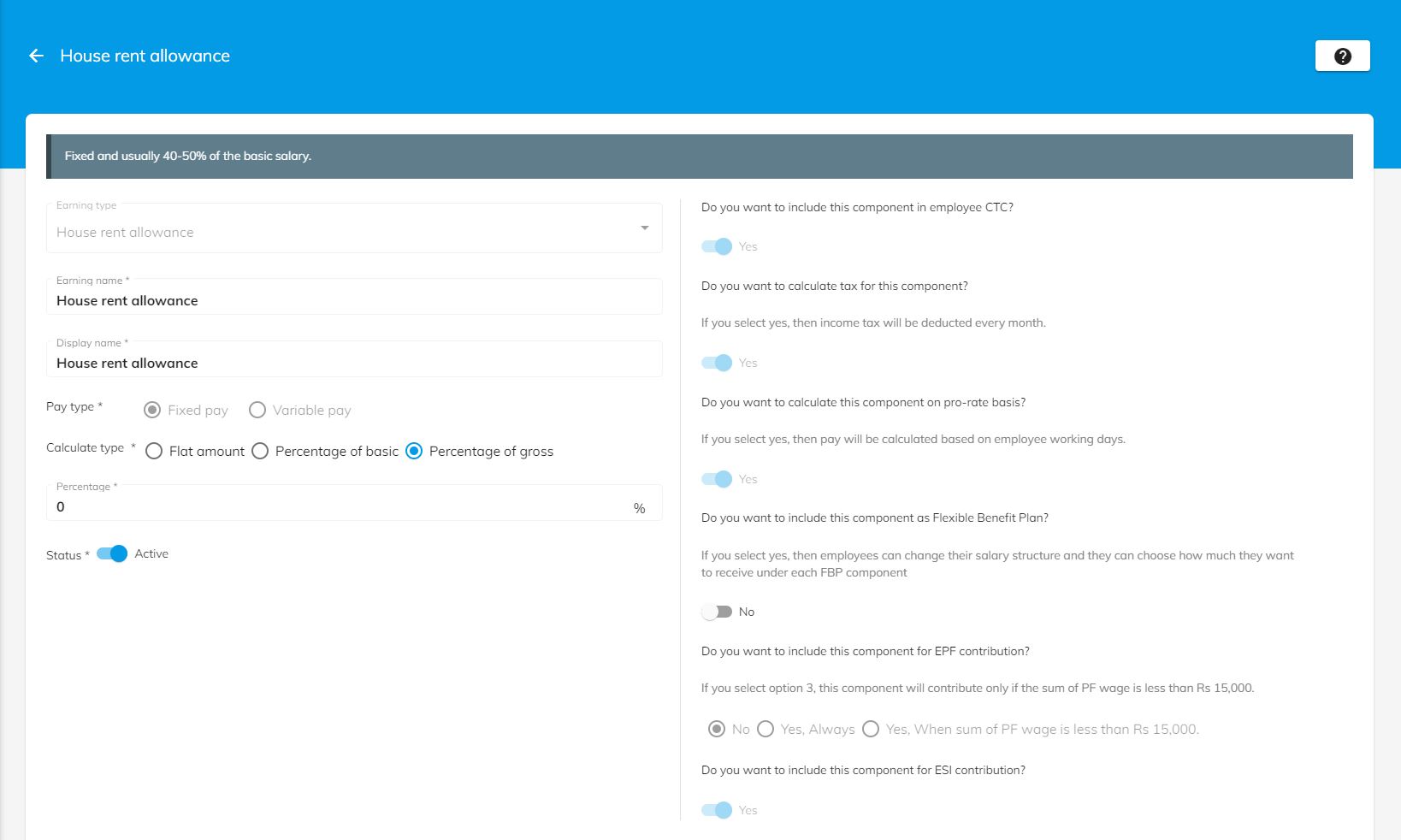

Let’s have a look at how the basic salary component is configured in OfficePortal. Here is the screenshot of the basic salary component under payroll settings.

HRA is by default configured as fixed pay and the calculation of HRA can be chosen as follows.

- A Flat Amount

- A percentage of CTC

- A percentage of gross

When you have selected any one of the above options, then you will be able to enter the required values in the below column and right now it is displayed as 50% since the percentage of CTC has been selected above. The percentage can be edited as per the CTC structure of the user’s preferences likewise for the remaining other two options. But you have to make sure that this component is not used in any of the employee’s salary details otherwise it will be non-editable.

The right-side pane shows the calculations using HRA in different statutory compliances such as Income Tax (TDS), ESI, and the pro-rate calculation based on attendance.

As per Indian statutory compliance, PF wage is calculated except for the HRA component. So the HRA component is not included in the PF wage calculation by default.

Conclusion #

In conclusion, HRA, or House Rent Allowance, is an important component of the Indian payroll that provides several benefits to both employees and employers. It can help to reduce the tax liability of employees, save on the cost of providing housing, retain talent, and improve employee satisfaction. However, administering HRA in Indian payroll also comes with some challenges and drawbacks, including eligibility criteria, documentation requirements, calculation methodology, tax implications, and market fluctuations.

To effectively administer HRA in Indian payroll, companies should follow best practices such as maintaining accurate documentation, communicating the policy clearly to employees, making timely payments, regularly reviewing the policy, ensuring compliance with regulations, and proper record keeping. It is also important for companies to carefully manage the challenges and drawbacks of HRA and implement effective policies and procedures to mitigate their impact.

Overall, HRA can be a valuable component of the Indian payroll when administered effectively and efficiently. By following best practices and managing the challenges and drawbacks, companies can provide a valuable benefit to their employees while also improving their financial health and compliance with regulatory requirements.

Click here to learn more about OfficePortal Payroll Software.